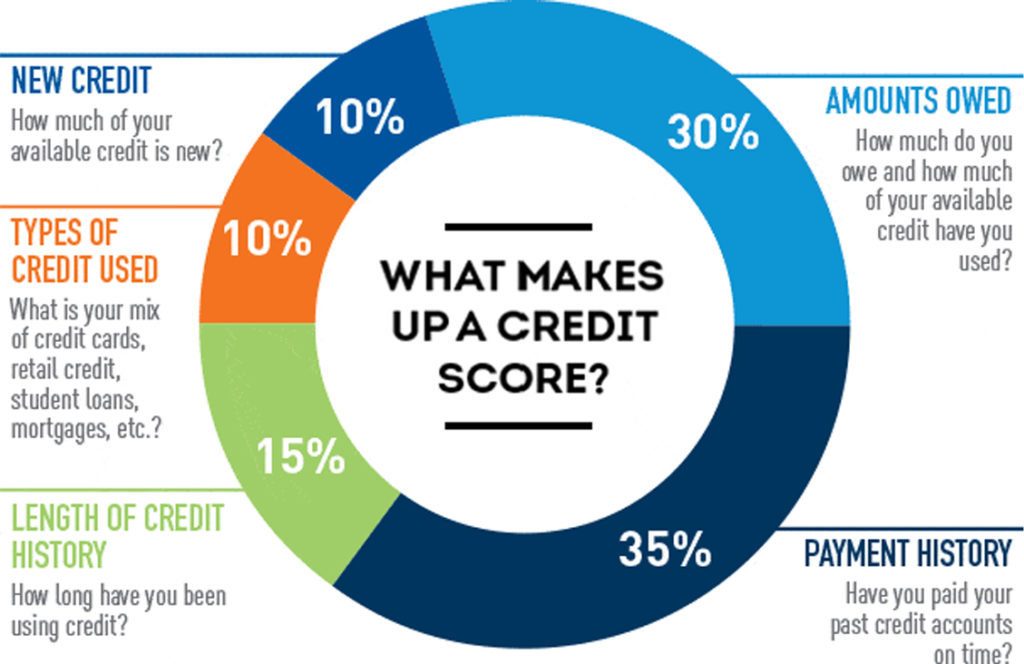

WHY CREDIT MATTERS

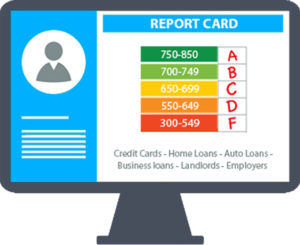

GRADING SYSTEM

Think of your credit score as a report card. The better the score, the higher grade you will receive from creditors, lenders, landlords and even potential employers.

A good credit score is used for more than just getting a credit card or a loan. Credit scores demonstrate your history of paying your debts to entities that loan you money.

SAVING MORE MONEY

Having good credit can potentially save you hundreds, if not thousands of dollars each year on your home loan, credit cards, auto loan, auto insurance, and even when applying for a rental property.

Let’s look at a few examples below to help illustrate the potential savings.

BUYING OR REFINANCE HOME LOAN

Higher credit scores can help you to qualify for lower interest rates on your mortgage loan. When you take out a mortgage to finance the purchase of a home, the interest you are charged can add up to tens of thousands of dollars over the course of the loan. Same applies when refinancing your existing mortgage.

For Example:

640 FICO Credit Score

30-yr mortgage for $350,000, you may pay 5.7% interest, depending on a few other factors. At 5.7% interest, your payment would be about $2,035 / month. Over the life of the loan, you would pay more than $383,000 in interest.

760 FICO Credit Score

With the same case scenario above, you might pay somewhere around 4.1% interest for the same 30-yr mortgage loan. At 4.1% interest, your payment would be about $1,700 / month. Over the life of the loan, you would pay a little over $260,000 in interest.

Total Savings

When compared with a low-score borrower, a high credit score could save you $335 per month in the example above. That adds up to more than $120,000 saved over the course of a 30-yr mortgage.

CREDIT CARDS

By having higher credit scores, you’re more likely to qualify for better interest rates, lower fees and better terms from credit card issuers. Lower interest rates equals to more saving.

If you have an existing credit card debt, can qualify for a low-rate or 0% balance transfer credit card. You’re more likely to qualify for one of these financing offers if your credit scores are good.

Some of the best reward credit cards feature amazing benefits which could net you a free travel, cash back, sign up bonus and other attractive perks. However, you’ll need good credit scores (sometimes excellent scores) if you want to take advantage of the best deals available.

AUTO LOANS & INSURANCE

The interest rate you’ll get depends on your credit score and income. Typically, borrowers with high credit scores get the best interest rates and terms. If you have a low credit score you will likely have to pay a higher interest rate or worse, your loan application could be rejected.

If your credit score is in very good, it is highly likely that you will receive a lower interest rate, which is great, because you will pay a lower amount of interest over the life of the loan, putting more money back in your pocket.

Most states let auto insurers weigh credit scores when setting rates. Lower the credit score can mean higher cost for auto insurance coverage.

APPLYING FOR A RENTAL PROPERTY

Looking to apply for an apartment, condo, townhome or house? Landlords or Property Managers will require a credit a report. Good to excellent credit could help differentiate you from the crowd of applications, while poor credit could rule you out.

Often times, people with low credit scores will be required to put a higher security deposit or even pay a higher monthly rate.

STARTING A NEW BUSINESS

Most business startups require a sizable amount of cash that you might not have available. In that case, you’ll need to obtain a small business loan. If your score is between 300 and 629, there’s a good chance the banks could reject your small-business loan application. Bad credit could limit your funding and make it that much harder to get your business up and running.

Unless, you have good to excellent credit, expect to pay a higher interest rate with not the best terms.

GETTING HIRED

Many employers conduct credit checks as part of the hiring process, especially for jobs involving access to money, sensitive customer data or company information. If you haven’t demonstrated financial responsibility, a prospective employer might be hesitant to hire you.

In some cases, employers have been known to check credit scores before giving a promotion or raise.

Recent Comments